How to get 10% more when you add funds to your Apple ID

If you're the type of person who regularly purchases music, apps, and other Apple ecosystem purchases, we'll show you how to get the most bang for your buck. Here's how you can earn an extra 10% when adding funds to your Apple ID through July 31.

An occasional promotion has been relaunched by Apple, providing those who added credit to their Apple ID.

Purchases will add an extra 10% on top whenever someone adds funds to their Apple ID, worth up to $200 in the United States, 200 GBP in the United Kingdom, and up to 300 euro in some European territories.

The bonus will only be applied to one purchase, according to the terms of the offer. That means that each user will only be able to get the 10% bonus the first time they add funds during the promotional period. This most recent offer stands until July 31, 2020, with users' eligibility varying based on their account information and purchase history.

An occasional promotion has been relaunched by Apple, providing those who added credit to their Apple ID.

Purchases will add an extra 10% on top whenever someone adds funds to their Apple ID, worth up to $200 in the United States, 200 GBP in the United Kingdom, and up to 300 euro in some European territories.

The bonus will only be applied to one purchase, according to the terms of the offer. That means that each user will only be able to get the 10% bonus the first time they add funds during the promotional period. This most recent offer stands until July 31, 2020, with users' eligibility varying based on their account information and purchase history.

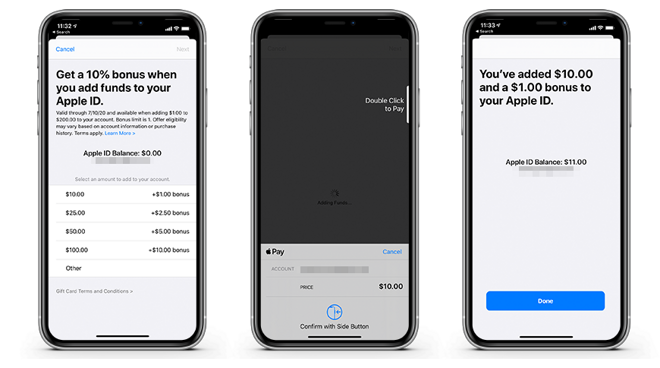

How to add funds to your Apple ID

- On your iPhone, open Settings

- Tap iTunes & App Store

- Tap Apple ID

- Tap View Apple ID

- Tap Add funds to Apple ID

- Add your funds, and then confirm your purchase.

Comments

I mean, I guess it depends on how long it's going to be "sitting around"? If you regularly spend $10–$25 (or more) on Apple services, this is free money.

If you put $100 on your Apple ID plus the $10 bonus and used it in three months the APR is 40%. If you take a year to spend it the return is still 10%. That seems like a waste to you?

In the politest way possible I can say it to you, you don't have any idea what you are talking about or are as uneducated about simple personal and consumer finance as someone can be.

Based on your comments, I don't think you actually like saving money and earning high quality returns on your investments. You compare this Apple ID $ program that pays a 10% bonus to debit cards and store cards that have a 0% return. What you've said makes no sense at all.

https://www.investopedia.com/ask/answers/whats-the-smallest-number-shares-i-can-buy/

What a great return!