Here's how Apple Card Daily Cash works

We now know exactly when you'll get your Daily Cash -- and it is not daily. And, here's what happens if you ever return an item that got you a cash reward.

You can check your Daily Cash rewards at any time

With Apple Card slowly rolling out to more users, Apple has been busy preparing a slew of support documents that explain how to use the new credit card -- and it includes explanations of many things we'd been left wondering. Such as precisely how Daily Cash works.

This is the system whereby if you buy something using your Apple Card, you get rewarded with a certain percentage of the purchase price paid back to your account in cash.

If you're buying something from Apple itself, that amount is 3%. If you buy anywhere else and use Apple Pay -- online or by waving your iPhone or Apple Watch in store -- you get 2%. And if you have to slum it by using the physical Apple Card, you'll get 1%.

These percentage figures are not astounding, but they become compelling when you know how you actually get this money. Plus, these amounts do add up. If you buy the base 13-inch MacBook Pro at an Apple Store or via Apple online, for instance, you'll get back $38.97 of the $1,299 sticker price.

Go for an iMac Pro and absolutely max out the specifications, and buying via Apple Card could get you $441.81 back.

Other cards can pay you more back, but they might come with other complications and limits, such as being 5% but only during your first three months.

If Apple Card's rewards are unexciting, they're still money coming your way, and where Apple wins is in how that is done. Instead of getting some points at the end of the month, Apple delivers actual money and right from the start, it's promised that you get this every day.

"Once a purchase is settled, your Daily Cash is added to your Apple Cash card," says Apple.

So it won't be that you turn away from the merchant's card reader and find you've got cash from Apple right then. Whenever the merchant finishes taking your money, though, that's when you get your cash back.

You get a notification whenever you've made a purchase, but you don't get a notification every time you receive Daily Cash. Instead, every morning you will get a notification of the total of Daily Cash received the day before, plus what your total is this month.

Then every Sunday, you get a notification that tells you your weekly spending and Daily Cash. There's a similar notification at the end of the month.

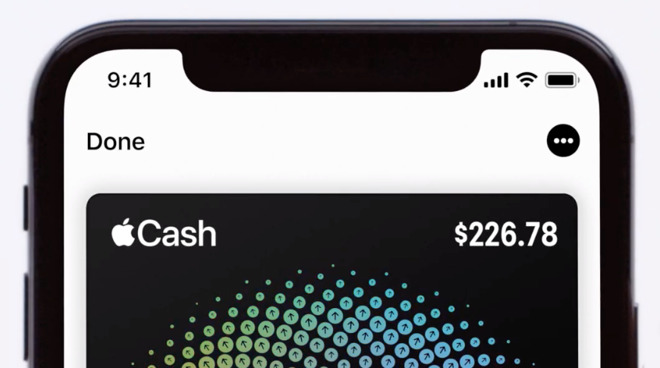

Alongside all this, you can check to see how much you've got back at any moment by going into the Wallet app on your iPhone.

You can see a Daily Cash amount for any individual transaction, plus a total received for that day and month.

However, you don't have to have an Apple Cash account if you don't want one for some reason. If you do not, you still get Daily Cash -- you just can't see what it is. It keeps on accruing and you can get an Apple Cash account at any time.

That Apple Cash account can be locked or restricted if there is some security issue. Even then, though, your Daily Cash amount continues to grow, as you talk to Apple about fixing whatever the problem is.

Except no, that's not what happens.

"If you return a purchase made with Apple Card, you are refunded the purchase price," says Apple. "The Daily Cash you received when you made the purchase is charged back to your Apple Card."

That just means that it will be more practical to use your Daily Cash at the end of a month rather than be going in to it every minute or every day.

The fact that you can, though, is part of this business of Apple making the entire credit card system simpler. When you don't have to choose between waiting for a bill at the end of the month or schlepping through some bank's complex online system, you will check your account more often.

When you check it regularly, you're always much more on top of your spending, and it's features like this that mean Apple Card could be good for us. It's still a credit card, so let's not get carried away, but the benefits of speed and simplicity make this attractive even if you could get more money with another card.

Keep up with AppleInsider by downloading the AppleInsider app for iOS, and follow us on YouTube, Twitter @appleinsider and Facebook for live, late-breaking coverage. You can also check out our official Instagram account for exclusive photos.

You can check your Daily Cash rewards at any time

With Apple Card slowly rolling out to more users, Apple has been busy preparing a slew of support documents that explain how to use the new credit card -- and it includes explanations of many things we'd been left wondering. Such as precisely how Daily Cash works.

This is the system whereby if you buy something using your Apple Card, you get rewarded with a certain percentage of the purchase price paid back to your account in cash.

If you're buying something from Apple itself, that amount is 3%. If you buy anywhere else and use Apple Pay -- online or by waving your iPhone or Apple Watch in store -- you get 2%. And if you have to slum it by using the physical Apple Card, you'll get 1%.

These percentage figures are not astounding, but they become compelling when you know how you actually get this money. Plus, these amounts do add up. If you buy the base 13-inch MacBook Pro at an Apple Store or via Apple online, for instance, you'll get back $38.97 of the $1,299 sticker price.

Go for an iMac Pro and absolutely max out the specifications, and buying via Apple Card could get you $441.81 back.

Other cards can pay you more back, but they might come with other complications and limits, such as being 5% but only during your first three months.

If Apple Card's rewards are unexciting, they're still money coming your way, and where Apple wins is in how that is done. Instead of getting some points at the end of the month, Apple delivers actual money and right from the start, it's promised that you get this every day.

Daily Cash

What we know now, though, is that you don't even wait a day for it. Daily Cash is not paid into your account at midnight or some other specific time, it is paid to you all day."Once a purchase is settled, your Daily Cash is added to your Apple Cash card," says Apple.

So it won't be that you turn away from the merchant's card reader and find you've got cash from Apple right then. Whenever the merchant finishes taking your money, though, that's when you get your cash back.

You get a notification whenever you've made a purchase, but you don't get a notification every time you receive Daily Cash. Instead, every morning you will get a notification of the total of Daily Cash received the day before, plus what your total is this month.

Then every Sunday, you get a notification that tells you your weekly spending and Daily Cash. There's a similar notification at the end of the month.

Alongside all this, you can check to see how much you've got back at any moment by going into the Wallet app on your iPhone.

You can see a Daily Cash amount for any individual transaction, plus a total received for that day and month.

Where the money goes

Daily Cash is paid into your Apple Cash account, an account that is separate from your Apple Card one but is accessed through your Wallet the same way.However, you don't have to have an Apple Cash account if you don't want one for some reason. If you do not, you still get Daily Cash -- you just can't see what it is. It keeps on accruing and you can get an Apple Cash account at any time.

That Apple Cash account can be locked or restricted if there is some security issue. Even then, though, your Daily Cash amount continues to grow, as you talk to Apple about fixing whatever the problem is.

When the money goes back

If we were more criminally-minded, maybe it would've occurred to us to buy a Mac Pro, immediately return it for a full refund and then make off with $883.62. (That's twice the 3% we got back via Apple Card, because the store refunds the entire purchase amount.)Except no, that's not what happens.

"If you return a purchase made with Apple Card, you are refunded the purchase price," says Apple. "The Daily Cash you received when you made the purchase is charged back to your Apple Card."

That just means that it will be more practical to use your Daily Cash at the end of a month rather than be going in to it every minute or every day.

The fact that you can, though, is part of this business of Apple making the entire credit card system simpler. When you don't have to choose between waiting for a bill at the end of the month or schlepping through some bank's complex online system, you will check your account more often.

When you check it regularly, you're always much more on top of your spending, and it's features like this that mean Apple Card could be good for us. It's still a credit card, so let's not get carried away, but the benefits of speed and simplicity make this attractive even if you could get more money with another card.

Keep up with AppleInsider by downloading the AppleInsider app for iOS, and follow us on YouTube, Twitter @appleinsider and Facebook for live, late-breaking coverage. You can also check out our official Instagram account for exclusive photos.

Comments

As a simple cash back credit card, there are several better, but as an icon of membership in the Apple Fan Club, there are no equals.

I really like this card but even though I’m a proud member of the Apple Fan Club I don’t see any visible display of its iconography to the general public so for that it’s not worth much. Maybe if it came with a t-shirt :-)

What I do think makes it at least equal and imo better than other cards is the simplicity of the enrollment process, lack of punishing fees, a clear and automatic detailing of its transactions, simplistic cash back rather than a complicating game of points, these are better than any card I’ve ever applied for. He

And by having the card automatically associated with Apple Pay will, I believe, increase the use of highly secured Apple Pay credit card transactions here in the US.

While others talk about how they get the same 2%, like from Capital One's Double Rewards Card, but then they fail to note that it's 1% only after the charge cycle is over and then then the other 1% only after you've paid off that balance.

Then there are other cards, like Cit Costco, which is great for 5% back on already low-cost fuel (up to $7000 per year) but you have to wait to redeem it annually. I have enough coming back on that card per year that it makes a really good dent in planning a great Summer vacation as the rewards are calendar year and they are dished out around February. I'm still considering adding all my CE purchases to it because they offer years of extended warranties to all CE purchases regardless of where you've bought it providing you used your Citi Costco CC.

The rate currently ranges from 12.99% to 23.99%. This is clearly stated on the first page of the customer agreement in LARGE BOLD TYPE.

At least here in the USA, interest rates are often based on the prime lending rates, like most consumer credit cards. When the prime lending rate changes, the card issuing bank does not need to revise their terms or customer agreement. It's already written in and you agreed to it.

I will bet you a buffalo nickel that the prime lending rate when you applied for your Barclaycard was lower than it is today. I will bet you another buffalo nickel that your Barclaycard terms state that the interest rate is variable.

The rates for some loans are fixed like fixed-rate mortgages versus ARMs, maybe your auto loan, maybe your student education loan.

Read your loan agreement for details. Clearly you have failed to do so.

I called Apple and found out that using that information is just like using the physical card which only gets you 1%. That was disappointing. I have the Citi Double Cash where I get 2% for everything I charge so I am sticking with that card until ApplePay is activated at different websites.

The Apple Credit card transaction details and the information provided are a plus for Apple but I want my two percent.

I still ordered the titanium card card just for kicks

It is very explicitly stated in the Apple Card customer agreement provided by Goldman Sachs. The banking industry is heavily regulated and these sort of details must be clearly disclosed to consumers.

Like Soli, you failed to pay attention. Being lazy does not exempt you from the customer agreement that you accepted.

You refer to details like your rate going up despite not receiving some sort of notification [sic].

Regardless of whether you pay your statement balance or the current balance due is irrelevant to whether or not Barclaycard changes your rate.

Have a great evening weeping about your credit card rate increase. My credit cards' interest rates change regularly but you won't see me grubbing for sympathy.

I will bet you another buffalo nickel that you aren't the center of the universe.

PS: You really need to learn how to use “[sic]” properly.

Check your math. There is no doubling involved. If this worked (which, as you point out, it wouldn’t). You would “just” end up with your money back from the purchase plus the 3% Apple Cash rebate.

All the people who say "this card isn't special" are mostly correct, and the same statement applies to all the other cards that are claimed to be "better" than the Apple Card. By themselves, they aren't "special", but each is special if one uses it in a manner that maximizes the rewards, e.g. for the Apple Card, shop at Apple or use Apple Pay, and then pay the statement balance every month. Just like every other such card.